{kind=link}

Is keeping nearly all your stocks in U.S. companies a smart move or a blind spot?

Most investors lean domestic, but that choice can leave you exposed if the U.S. stumbles.

In this post I’ll explain a simple rule: target about 20% to 40% of your stock holdings in international equity (foreign stocks).

Where you land in that range depends on your age, how much of your life ties to the U.S., and how much volatility you can stomach.

Follow the guidance here and you’ll get real diversification without overcomplicating things.

Recommended International Equity Allocation Ranges for a Diversified Portfolio

Most investors should aim for 20% to 40% of their total stock holdings in international equity. That range comes from Vanguard’s research and reflects what the global market actually looks like. The U.S. makes up roughly 65% of world equity markets right now, leaving about 35% outside U.S. borders. If you went purely by market cap, you’d put around 35–40% international. But the average U.S. investor only holds about 20%, which creates home-country concentration risk. Staying inside that 20–40% corridor gives you real diversification without going so far that you’re ignoring what most institutions consider sensible.

Where you land in that range depends on your risk tolerance, how long you have until you need the money, and how much U.S. economic exposure you already have through your job and other assets. Conservative investors who are near or in retirement often stick to 10–20% international. They’re trying to avoid currency swings and foreign-market volatility when they’re spending down what they’ve saved. Moderate investors who want balanced global exposure usually end up around 25–35%. Aggressive or globally minded investors may push 35–40%, accepting extra short-term volatility in exchange for broader diversification. Going much below 20% keeps you heavily tied to one country’s fortunes. Going much above 40% increases currency risk without a clear long-term diversification benefit for U.S.-based investors.

If you hold 80% or more of your total equity in one country while also earning income in that country and holding your bonds there, you’re not diversified in any meaningful sense. A practical rule is to check where you fall in relation to the market-cap baseline, then adjust based on what matters most to your situation.

Quick numeric allocation targets:

- Conservative (lower volatility preference, near retirement): 10–20% international equity

- Moderate (balanced diversification): 25–35% international equity

- Market-cap baseline (track the global opportunity set): ~35% international equity

- Aggressive / global tilt: 35–40% international equity

- Developed vs. emerging split inside international: roughly 70–85% developed / 15–30% emerging

Understanding the Role of International Equity in Portfolio Diversification

Holding international equity means you’re spreading your bets across different economies, currencies, and industry mixes instead of relying on a single country’s stock market. The U.S. currently makes up about 65% of the global equity market, but the average U.S. investor puts roughly 80% of their stock portfolio in domestic companies. That gap creates a home-bias problem. When one market or sector leads in one decade, another often leads in the next. Diversifying across countries helps smooth those swings and reduces the risk of having all your money in the wrong place at the wrong time.

Different countries lead in different years. In the 2000–2010 “lost decade,” the S&P 500 delivered nearly flat returns while resource-rich countries like Australia, Brazil, and Canada outperformed U.S. stocks by significant margins.

Concentration risk is real and can show up quickly. In June 2024, Nvidia became the world’s largest publicly traded company, and its rise materially changed U.S. index returns over the prior two years. Removing just that one stock from the calculation would have made U.S. returns lag some foreign markets around the 2022 trough. Holding international equity limits how much any single company or country can dominate your results. It keeps you exposed to growth and profits wherever they happen to occur.

| Region | Period of Outperformance |

|---|---|

| Non-U.S. developed & emerging | 2000–2010 |

| U.S. equities | 2010–2020 |

| Varied (sector-dependent) | 2020–2025 |

Factors That Should Adjust Your International Equity Percentage

Your ideal international allocation shifts based on a handful of personal factors that change how much foreign uncertainty you can afford to take on. Retirement stage is one of the biggest. If you’re spending down assets and paying bills in U.S. dollars, currency swings become painful in the short term. Many retirees reduce international exposure to 10–20% to limit that volatility. Younger investors with 20 or 30 years until they need the money can usually handle the extra ups and downs and may comfortably target 30–40% international. Time smooths out currency noise, but only if you have enough of it.

Income and economic ties matter just as much. If you earn a U.S. salary, own U.S. real estate, and hold U.S. bonds, you already have heavy exposure to the U.S. economy. Increasing international equity percentage offsets some of that home-country concentration. On the flip side, if your job depends heavily on global trade or foreign revenue, you might already carry implicit international exposure and may choose a lower allocation. Tax considerations also factor in. Foreign dividends may face withholding taxes that reduce after-tax returns, though in many cases you can claim a foreign tax credit. If the tax drag is significant and you can’t fully offset it, you might trim international exposure slightly to preserve net returns.

Your currency spending plans and broader asset allocation also influence the right number. If all your bonds are U.S. Treasuries and you want to keep a stable relationship between your bond hedge and your stock risk, adding a large international equity position can break that balance. International stocks correlate differently with U.S. bonds than U.S. stocks do. Some investors add international fixed income to maintain the hedge, but that adds complexity and cost. If you want to keep it simple, moderate your international equity percentage to a level where your existing bond holdings still provide effective risk offset.

Six factors to weigh when setting your international equity percentage:

- Age and time horizon (younger = higher tolerance for foreign volatility)

- Income source and currency exposure (U.S.-based salary = already U.S.-heavy)

- Retirement stage (near or in retirement = lower international allocation)

- Tax treatment of foreign dividends (withholding and credit availability)

- Bond allocation and hedge structure (U.S.-only bonds favor lower international equity)

- Comfort with currency risk and political/regulatory uncertainty

Deciding How Much to Allocate to Developed vs. Emerging Markets

Inside your international equity bucket, you need to decide how much goes to developed markets (Europe, Japan, Australia) and how much goes to emerging markets (China, India, Brazil). A typical split is 70–85% developed and 15–30% emerging, roughly mirroring the composition of broad international indexes. Developed markets have more mature economies, deeper capital markets, and generally lower volatility than emerging markets. Emerging markets offer exposure to faster-growing economies but come with higher political risk, weaker regulatory frameworks, and bigger price swings.

Many investors are tempted to overweight emerging markets because they expect faster GDP growth in countries like China and India. This is the “growth trap.” High expected growth is usually already priced into stock valuations, and emerging-market equities often underperform developed markets over multi-decade stretches despite faster economic expansion. Increase your emerging-market allocation for diversification and to capture different industry and currency exposures, not because you think you’ve identified the next decade’s winners. If you choose to tilt more aggressively, accept the higher volatility and the real possibility of lagging U.S.-heavy portfolios for years at a time.

Sample developed/emerging splits by risk profile:

- Conservative international: 80% developed / 20% emerging (example: 24% developed + 6% emerging out of a 30% total international allocation)

- Moderate international: 75% developed / 25% emerging (example: 22.5% developed + 7.5% emerging out of a 30% total international allocation)

- Aggressive international: 65–70% developed / 30–35% emerging (example: 21% developed + 9% emerging out of a 30% total international allocation)

Currency Risk and Hedging Choices in International Equity Allocation

When you own international equity, you’re also owning the foreign currency in which that stock is priced. If the euro or yen weakens against the dollar, your return in dollar terms shrinks even if the stock price itself went up. The reverse is also true. A strengthening foreign currency can boost your dollar return. Over long time periods, currency effects often cancel out, but they can materially change your results over any given three to five year stretch. Currency risk becomes more important the closer you are to needing the money, which is why many retirees reduce international exposure or consider hedged funds.

Hedging reduces currency volatility but adds cost and can dampen diversification benefits. Currency-hedged international equity funds cost more to run due to the ongoing hedging transactions, and those costs come out of your return. Hedging also removes some of the diversification advantage. If the dollar surges during a U.S. stock sell-off, unhedged foreign holdings may provide a partial offset. For long-term equity investors, staying unhedged is the norm because currency moves wash out over decades and hedging costs add up. Shorter-term investors or those who plan to spend in dollars soon may prefer hedged exposure to lock in smoother results.

Your choice between hedged and unhedged funds influences how much international equity you hold. If you stay unhedged and accept currency swings, you may choose a slightly lower international allocation to keep total portfolio volatility in check. If you hedge, you can lean toward the higher end of the 20–40% range because you’ve removed one layer of uncertainty. Either way, the decision should reflect how you plan to spend your money and how much short-term volatility you can handle without panicking.

Practical Implementation: Funds, Indexes, and Costs for International Exposure

Building international equity exposure is straightforward if you stick to low-cost, broad index funds. The most common approach is to use a total international equity fund that tracks an index like MSCI ACWI ex-USA, which covers both developed and emerging markets outside the U.S. in market-cap weights. If you prefer more control, you can split the allocation into separate funds: one tracking MSCI EAFE (developed markets in Europe, Australasia, and the Far East) and one tracking MSCI Emerging Markets. Either setup works. The single-fund approach is simpler, while the two-fund approach gives you more rebalancing flexibility and the ability to adjust your developed/emerging split over time.

Costs matter more than past performance when selecting funds. In one real-world comparison, one international fund had a 0.77% expense ratio and 54% annual turnover, while another offered a 0.32% expense ratio and 12% turnover. Lower expense ratios predict future outperformance more reliably than recent returns, and lower turnover reduces tax drag in taxable accounts. Favor index funds over actively managed funds unless you have a specific, evidence-based reason to expect the active manager will beat the market after fees. Over long periods, the majority of active international equity funds underperform their benchmarks net of fees.

Tax efficiency and account placement also affect your net returns. International equity funds generate foreign dividends that may be subject to withholding taxes, though you can often claim a foreign tax credit if you hold the fund in a taxable account. In tax-advantaged accounts like IRAs, you lose the credit but avoid U.S. tax on distributions. If your international holdings generate high turnover or dividend income, consider placing them in a tax-advantaged account to minimize drag. Keep an eye on your fund’s turnover ratio and distribution history when deciding where to hold it.

Total international equity funds simplify implementation and automatically maintain the developed/emerging split used by the underlying index. They also reduce the number of positions you need to monitor and rebalance. If you prefer granular control or want to tilt toward a specific region, you can use regional funds (Europe, Pacific, emerging markets) instead, but doing so increases the number of decisions you have to make and may increase your overall costs if you end up holding more funds than necessary.

Essential fund-selection criteria for international equity:

- Expense ratio below 0.20% for index funds (lower is better)

- Turnover ratio under 20% to minimize tax drag

- Broad index coverage (MSCI ACWI ex-USA, MSCI EAFE, MSCI EM)

- Fund structure (ETF vs. mutual fund) matching your trading and account type

- Tax efficiency and foreign tax credit availability in taxable accounts

Rebalancing Your International Equity Percentage Over Time

Markets don’t move in sync, so your international equity allocation will drift away from your target over time. U.S. stocks might outperform for a few years and push your domestic percentage higher, or non-U.S. markets might surge and increase your international slice. Rebalancing brings your allocation back to your chosen target and forces you to sell what went up and buy what lagged. It’s a disciplined way to avoid chasing recent performance. The standard rule is to rebalance at least once a year or whenever any allocation drifts more than 3–5 percentage points from your target.

Using separate regional funds (developed and emerging) instead of a single total international fund creates more rebalancing opportunities and can generate a small “rebalancing bonus” as you trim winners and add to losers within your international sleeve. That said, it also adds complexity and may increase transaction costs if you’re using ETFs with commissions or bid-ask spreads. For most investors, annual calendar rebalancing with a total international fund hits the sweet spot between discipline and simplicity.

Simple rebalancing rule in three steps:

- Set a target percentage (example: 30% international equity, 70% U.S. equity).

- Check allocations once per year or whenever a major market move happens.

- If any slice drifts more than 5 percentage points from target, rebalance by selling the overweight position and buying the underweight position.

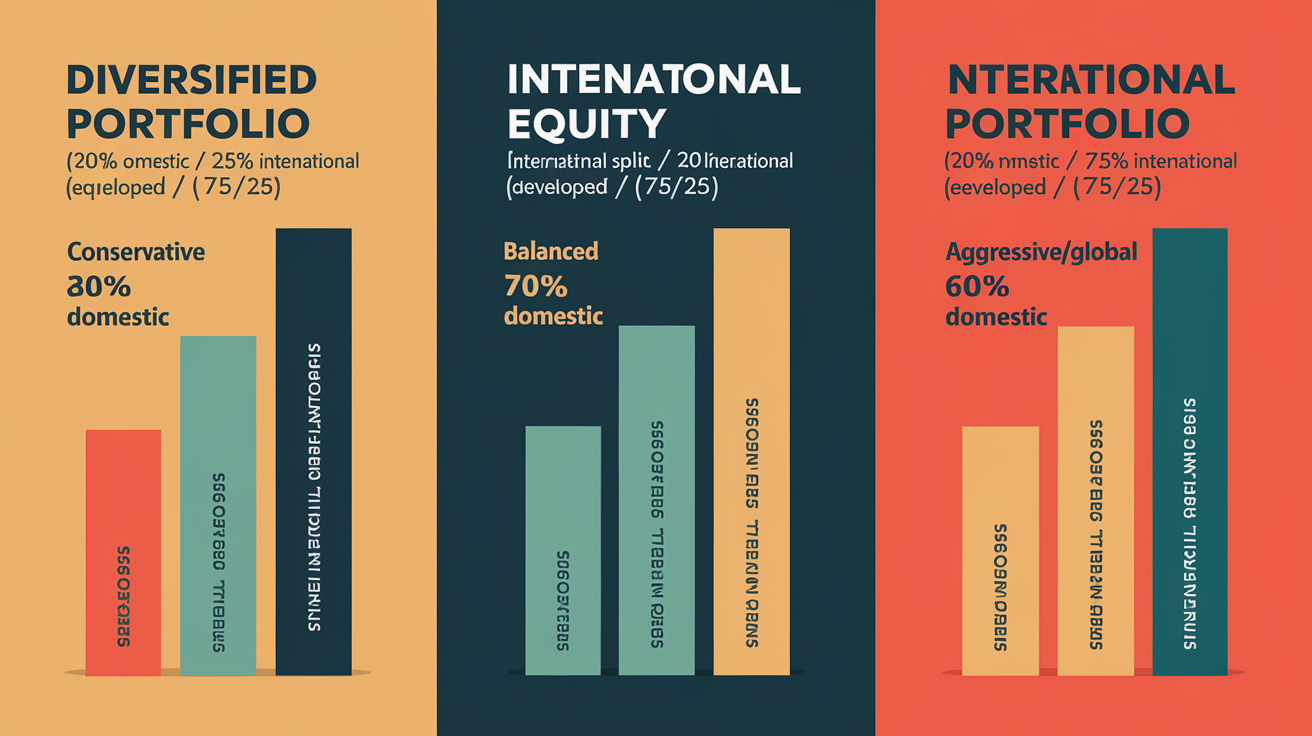

Sample Diversified Portfolio Splits Using Different International Equity Percentages

Concrete examples make the guidance easier to apply. A conservative portfolio might use 80% domestic equity and 20% international equity, with the international slice split 75% developed and 25% emerging. That translates to 80% U.S., 15% developed international, and 5% emerging markets. This setup minimizes currency risk and foreign volatility while still providing meaningful diversification. It fits retirees or investors who want smoother short-term results and already have substantial U.S. economic exposure through income and bonds.

A balanced portfolio shifts to 70% domestic and 30% international, maintaining the 75/25 developed/emerging split inside the international allocation. That gives you 70% U.S., 22.5% developed international, and 7.5% emerging markets. This is close to the market-cap baseline and works well for moderate-risk investors with a multi-decade time horizon who want global diversification without extreme tilts in any direction. It’s a practical default for many long-term savers.

An aggressive or globally minded portfolio might use 60% domestic and 40% international, again splitting the international bucket 75/25. The result is 60% U.S., 30% developed international, and 10% emerging markets. This allocation reduces home bias more dramatically and aligns more closely with true global market-cap weights, accepting higher short-term volatility and currency risk in exchange for broader geographic exposure. It makes sense for younger investors or those who are comfortable with foreign-market uncertainty and want to limit concentration in any single country.

| Portfolio Type | Domestic Equity % | International Equity % | Developed % | Emerging % |

|---|---|---|---|---|

| Conservative | 80% | 20% | 15% | 5% |

| Balanced | 70% | 30% | 22.5% | 7.5% |

| Aggressive / Global | 60% | 40% | 30% | 10% |

Final Words

You now have a clear numeric guide. Aim roughly 20–40% in international equity, with conservative near 10–20%, moderate 25–35%, and aggressive 35–40%. Also covered developed vs emerging splits, currency, fund choices, and rebalancing.

Pick a target inside the recommended range, choose low-cost funds that match your tilt, and set a rebalancing rule, annual or at 3–5 percentage points. Review the plan if your life or goals change.

Decide a number and stick to the process. That’s how much international equity to include in a diversified fund portfolio and it keeps your long-term plan on track.

FAQ

Q: How much of my portfolio should be in international equities?

A: How much of your portfolio should be in international equities depends on your risk and goals, but a practical range is 20–40% of your stock sleeve—10–20% if conservative, 25–35% moderate, 35–40% aggressive.

Q: What is the 7 3 2 rule?

A: The 7 3 2 rule is not a single, widely agreed standard; it’s a shorthand some people use for different allocation or timing ideas—always check the original source before applying it to your portfolio.

Q: What is the 70/30 Buffett rule investing?

A: The 70/30 Buffett rule refers to a simple split of roughly 70% stocks and 30% bonds; note Buffett’s own public advice often favors a heavier stock tilt for many investors, so adjust for your goals.

Q: Is 20% international stock too much?

A: Having 20% international stock is not too much; it’s a common, reasonable baseline that reduces home bias. Shift lower near retirement (10–20%) or higher (30–40%) if you’re younger and seek global exposure.