{kind=link}

What if your “set-it-and-forget-it” target-date fund is quietly changing how much risk you face, without you knowing?

Glidepaths are the preset schedules inside those funds that shift your mix from stocks to bonds as retirement nears.

Think of it like a dimmer switch that eases risk down over decades so one bad market year doesn’t derail your plan.

This post breaks down how glidepaths move, why they speed up near retirement, and the difference between “to” and “through” designs so you can pick the fund that fits your goals.

Core Explanation of Target-Date Fund Glidepaths

A target-date fund glidepath is basically a preset schedule that shifts your money from growth stuff (mostly stocks) to safer holdings (bonds and cash) as you get closer to retirement. Picture a dimmer switch that turns down risk over four decades. You’re 25 and retirement’s forever away? The fund might be sitting at 90% stocks. Fast forward to 64, and that same fund could be holding just 40% stocks with 60% in bonds. You don’t do anything. The fund rebalances itself.

Early on, glidepaths pack in the equities because you’ve got time to bounce back from market meltdowns and let compounding do its thing. That dollar you toss in at 25 has 40 years to grow, so short-term chaos matters way less than grabbing those higher long-term stock returns. Through your 30s and 40s, the glidepath starts easing toward bonds and fixed-income. The shift picks up speed in your 50s and early 60s, when a sudden crash could erase gains you won’t have time to replace.

This happens to protect you from sequence-of-returns risk. That’s the danger of a big drop right before or early in retirement locking in losses you can’t undo. The whole point of automation here is you don’t have to time the market or remember to rebalance every year. The glidepath handles it, keeping your portfolio lined up with your shrinking time horizon and pulling risk off the table as your retirement date creeps closer.

Five things driving the gradual risk pullback:

- Time horizon shrinkage gets you fewer years to recover from losses, so less room to hold volatile stuff.

- Human capital decline means your ability to earn future income drops as retirement nears, making your financial capital more precious.

- Longevity assumptions have glidepaths balancing growth needs against the chance you’ll outlive your money.

- Sequence-of-returns protection cuts equity exposure before retirement to shield you from catastrophic early losses.

- Behavioral guardrails stop you from panic selling or chasing performance at exactly the wrong moment.

Asset Allocation Mechanics Throughout the Glidepath

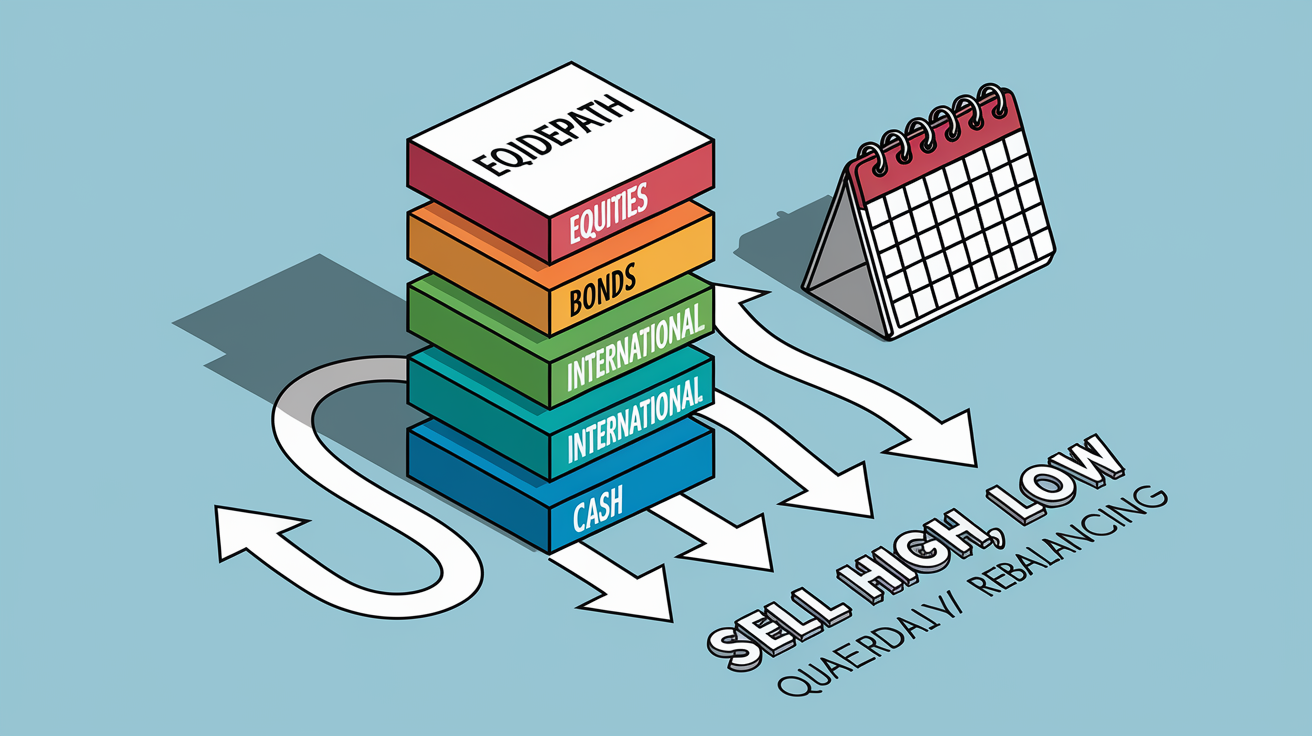

Glidepaths run on predefined rules that decide when and how fast to cut equity exposure. Most funds glide smoothly instead of jumping around, rebalancing every quarter or year to stay on track. The pace isn’t constant. Equity reduction often speeds up in the final 10 to 15 years before the target date, when you’ve got the most to lose and the least time to recover. Before that window, changes are gentler. Maybe one or two percentage points of equity reduction per year. Hit your 50s and the glidepath might cut equity by three or four points annually, moving faster to lock in gains and dial down volatility.

Here’s how it works. Each year, the fund manager checks the current allocation against the glidepath’s schedule. If equities have grown past the target because of market gains, the fund sells some stock and buys bonds to bring the mix back in line. If equities have dropped below target, it does the opposite. This automatic rebalancing forces a “sell high, buy low” discipline without you lifting a finger. The further out you are from retirement, the slower the glidepath moves. The closer you get, the faster risk comes off.

| Asset Class | Early-Career Allocation | Mid-Career Allocation | Near Retirement Allocation |

|---|---|---|---|

| Equities | 85–90% | 60–70% | 35–50% |

| Bonds | 10–15% | 30–40% | 50–65% |

| International Exposure | 30–40% | 25–35% | 15–25% |

| Cash/Short-Term Holdings | 0–5% | 0–5% | 0–10% |

Differences Between “To” vs. “Through” Glidepaths

Target-date funds split into two camps: “to” retirement and “through” retirement. A “to” glidepath hits its most conservative allocation right at the target date (say, the year you turn 65) and then stays put for the rest of your life. If the fund’s final mix is 40% stocks and 60% bonds, that’s where it parks from 65 onward. The assumption is you’ll roll your balance into something else at retirement, so the fund stops adjusting once you reach the target year. “Through” glidepaths keep cutting equity exposure after the target date, sometimes for 20 or 30 more years. They assume you’ll stay invested in the fund during retirement and keep drawing income from it, so the glidepath slowly de-risks further to protect against early-retirement market shocks.

The real difference is how much equity you’re holding at and after retirement. “To” funds usually land around 25–40% equity at the target date and freeze. “Through” funds might start at 50–55% equity at the target date, then glide down to 30% or lower by your mid-80s. This creates a tradeoff. Higher equity in early retirement gives you more growth potential to fight longevity risk, but it also means more volatility right when you’re starting to pull money out. “To” glidepaths deliver more stability at retirement but might leave you short if you live into your 90s and inflation eats away at your fixed-income returns.

Key differences between the two:

- Risk profile at retirement is more conservative in “to” funds, while “through” funds hold more equity at 65.

- Post-retirement behavior has “to” funds holding a static allocation and “through” funds continuing to reduce equity for decades.

- Longevity protection means “through” funds keep more growth potential while “to” funds prioritize stability over late-life growth.

- Withdrawal timing assumes you leave the fund at retirement with “to” and stay invested with “through.”

Comparing Glidepaths Across Major Fund Families

Vanguard, Fidelity, and T. Rowe Price all build target-date funds, but their glidepaths reflect different takes on risk, longevity, and how people actually behave. Vanguard’s pretty conservative. Its funds reach the target date with around 50% equity exposure, then glide down to roughly 30% equity about seven years into retirement and hold that mix from there. Vanguard assumes most people will stay invested in the fund during retirement, so it uses a “through” design that keeps de-risking after age 65. The focus is on protecting against early-retirement market crashes while still grabbing some growth to fight inflation over 20 or 30 years of retirement.

Fidelity goes more aggressive. Its Freedom Index target-date series lands at around 50–54% equity at the target date and sticks close to that level well into retirement, with only gradual reductions over time. Fidelity’s models assume participants need more growth to sustain withdrawals across longer lifespans, especially if Social Security and pensions replace less income than they used to. The higher equity allocation cranks up volatility but also raises the odds that your portfolio can keep up with inflation and healthcare cost growth in your 70s and 80s.

T. Rowe Price splits the difference. Its Retirement funds arrive at the target date with approximately 55% equity, then continue a slow glide to about 20–30% equity 30 years into retirement. The extended glidepath reflects an assumption that retirees will draw income from the fund for decades, and that a gradual equity reduction balances growth needs against the rising danger of poor market timing as you age. All three use “through” designs, but the speed and endpoint differ. Two people retiring the same year can end up with very different risk exposures depending on which fund family their employer picked.

| Fund Family | Equity at Target Date | Equity 10 Years After | Glidepath Style |

|---|---|---|---|

| Vanguard | ~50% | ~30% | Through (stabilizes ~7 years post-retirement) |

| Fidelity | ~50–54% | ~48–50% | Through (slow, gradual reduction) |

| T. Rowe Price | ~55% | ~40–45% | Through (extends up to 30 years post-retirement) |

Visualizing Glidepaths: How Allocations Change Year by Year

A standard glidepath chart puts equity allocation on the vertical axis and age or years-to-retirement on the horizontal. The equity line starts high on the left (often 85–90% when you’re in your 20s) and slopes downward as you age, ending somewhere between 30% and 55% at retirement depending on the fund’s design.

The curve’s usually not a straight line. It’s fairly flat in your 20s and 30s, meaning equity stays high and changes slowly. The slope gets steeper in your 40s and 50s, when the glidepath speeds up de-risking. The steepest part typically hits in the final 10 to 15 years before retirement, where equity might drop three to five percentage points per year. After the target date, “to” glidepaths flatten into a horizontal line (no more changes), while “through” glidepaths keep sloping downward for another 20 or 30 years. The bond allocation curve mirrors the equity curve, rising from 10–15% early on to 50–70% near or after retirement.

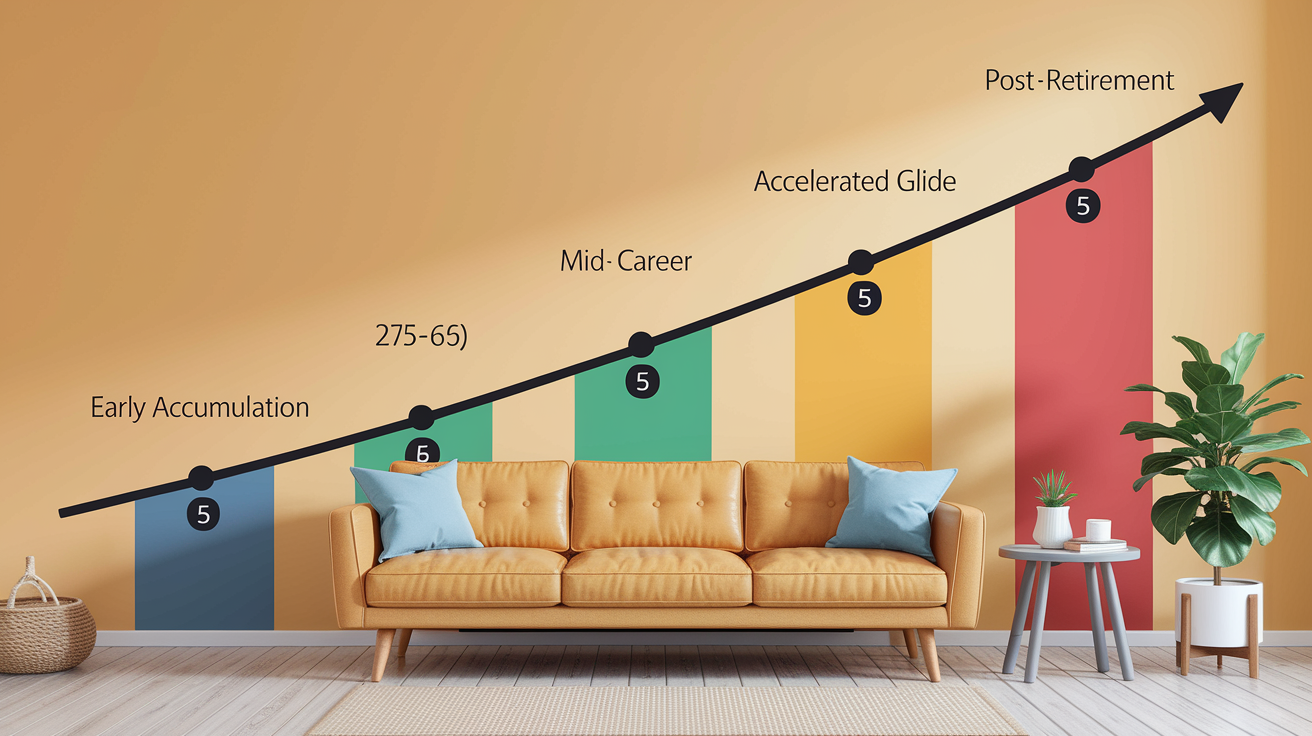

The progression breaks into five rough stages:

- Early accumulation (age 20–35) has equity near 90%, barely moving. Growth is the only goal.

- Mid-career plateau (age 35–50) drifts equity down gradually to 60–70%. Slow, steady de-risking.

- Accelerated glide (age 50–60) drops equity faster, maybe losing 3–4 points per year. The steepest part of the curve.

- Final approach (age 60–65) gets equity to target-date allocation (30–55%). Heaviest rebalancing activity.

- Post-retirement phase (age 65+) freezes “to” funds and keeps “through” funds gliding down to a terminal allocation 20–30 years later.

Risks and Benefits of Glidepaths

The biggest benefit is simplicity. You pick one fund, and it handles asset allocation, rebalancing, and risk management for the next 40 years without you making another decision. This automatic de-risking protects you from your own worst instincts. Panic selling after a crash or chasing hot sectors at the wrong time. Glidepaths also force a disciplined “sell high, buy low” pattern by trimming winners (stocks after a rally) and adding to losers (bonds after a selloff). For most people, especially those who don’t want to think about investing, this hands-off structure delivers better results than trying to time the market or fiddle with allocations based on headlines.

The main risk is glidepaths are generic. They assume you’ll retire at 65, live to 90, and pull out a steady 4% of your balance each year. If any of those assumptions is wrong (maybe you retire at 60, or you plan to work until 70, or you inherit money and don’t need growth), the standard glidepath might not fit. A one-size-fits-all equity curve can leave early retirees overexposed to market crashes or late retirees underexposed to growth. Glidepaths also can’t adapt if you change your mind. Market crashes when you’re 55 and you decide to work five more years? The fund keeps de-risking on schedule, locking in a conservative allocation right when you could afford to take more risk and ride the recovery.

Another risk is underperformance compared to a custom portfolio. If you’re willing to take more equity risk in retirement because you have other income sources, a generic “through” glidepath that drops to 30% equity by age 75 might cost you growth you could’ve captured. On the flip side, if you’re risk-averse or have health issues, a glidepath that holds 50% equity at retirement might feel too volatile. Glidepaths optimize for the average participant, not for you specifically. That’s the tradeoff. Maximum convenience, less personalization.

Final Words

We showed how target-date fund glidepaths work: equity-heavy early, gradually shifting into bonds and cash to reduce risk as retirement nears.

You also saw the mechanics behind allocation changes, the difference between “to” and “through” styles, how major providers vary, and the main risks and benefits.

Check how target-date fund glidepaths work for your chosen date, match the glidepath to your savings plan, and keep fees low.

Stick with the plan and you’ll be in better shape over time.

FAQ

Q: What is a target-date fund glidepath?

A: The target-date fund glidepath is the plan that shifts a fund’s mix from more stocks early to more bonds and cash as the target date nears, automating risk reduction over time.

Q: How do glidepaths work?

A: Glidepaths work by following set rules that lower equity exposure and raise bond and cash holdings as the target date approaches, helping smooth returns and reduce sequence-of-returns risk.

Q: Why do glidepaths move from equity-heavy to conservative holdings?

A: Glidepaths move from equity-heavy to conservative holdings because stocks support long-term growth, while bonds and cash protect capital as retirement nears, lowering the chance of large losses when you’ll need the money.

Q: What is the difference between “to” and “through” glidepaths?

A: The difference between “to” and “through” glidepaths is that “to” reaches a conservative mix at the target date, while “through” keeps shifting to even safer allocations after the target date into retirement.

Q: How does asset allocation change year by year in a glidepath?

A: Asset allocation changes year by year by steadily cutting equities and boosting bonds; the equity reduction often accelerates in the final 10–15 years before the target date to reduce downside risk.

Q: What are the main drivers behind gradual risk reduction in a glidepath?

A: The main drivers behind gradual risk reduction are time horizon, income needs at retirement, sequence-of-returns risk, individual risk tolerance, and the fund’s design or regulatory limits.

Q: How do glidepaths differ across Vanguard, Fidelity, and T. Rowe Price?

A: Glidepaths differ across Vanguard, Fidelity, and T. Rowe Price because each provider chooses different equity levels at the target date—some stay around 50% equity, others cut equity much lower—reflecting different risk views.

Q: What are the benefits and risks of using a glidepath?

A: The benefits of using a glidepath are simplicity, automatic rebalancing, and steady risk reduction; risks include a poor fit with your personal needs and possible underperformance if your retirement timing changes.

Q: How should I pick a target-date glidepath for my situation?

A: You should pick a target-date glidepath by matching its risk path to your time horizon, income needs, and comfort with stock drops; choose a more conservative glidepath if you’ll need the money soon.