{kind=link}

What if owning a slice of a $50 million property was as simple as buying a song online?

Tokenized investment funds turn fund shares into blockchain tokens so ownership, transfers and recordkeeping happen on a ledger instead of paper.

That means smaller minimums, faster settlement, and clearer records, often without changing the fund’s economic rules.

This intro explains what tokenized investment funds are, how they work (from token issuance to custody and trading), and the practical benefits and risks investors should know before they buy a tokenized fund share.

Clear Overview of Tokenized Investment Funds and Their Core Mechanics

Tokenized investment funds represent ownership shares of an investment fund as digital tokens on a blockchain. Instead of paper certificates or entries in a traditional registry, your fund units exist as cryptographic tokens that keep the fund’s economic structure intact (dividends, voting rights, redemption terms) while moving ownership records and operational tasks onto a distributed ledger. The global investment fund industry manages roughly USD 147 trillion in assets under management as of mid-2025. Tokenization is trying to modernize infrastructure that hasn’t changed much in decades.

Here’s how tokenized funds work: a fund manager picks an asset or portfolio and issues blockchain tokens that map to fund shares or unit classes. Each token creation event gets recorded on-chain, and all subsequent transfers, subscriptions and redemptions are logged on an immutable ledger for real-time reconciliation. Smart contracts automate subscriptions, redemptions, corporate actions and recordkeeping, cutting manual reconciliation and shortening execution timelines. Secure on-chain price feeds (delivered by oracles) publish net asset value (NAV) data so that valuation and automated settlement can happen almost instantly. Atomic delivery-versus-payment (DvP) workflows synchronize the asset and payment legs across traditional and blockchain rails, cutting settlement risk.

Tokenized fund shares can be transferred 24/7 (subject to regulatory and fund-specific transfer restrictions) and can interact programmatically with other on-chain systems. Fractional ownership is built into the token design: naturally divisible tokens lower minimum investment thresholds and broaden access to high-value or illiquid assets such as private equity, real estate and infrastructure. This article was last updated on February 12, 2026, reflecting regulatory milestones through January 2026 and market developments through November 2025.

Types of Tokenized Investment Funds and What Can Be Tokenized

Tokenization isn’t limited to a single asset class or fund type. Any investment vehicle that can be legally structured and valued can issue tokens to represent ownership interests. Fund categories fall into three broad buckets: public tokenized funds include tokenized exchange-traded funds (ETFs), mutual funds and money market funds designed for broad participation and regulated under existing public-fund frameworks. Private tokenized funds cover tokenized private credit, venture capital, private equity, hedge funds and real estate funds, often restricted to accredited or institutional investors, and use tokenization to enable fractional ownership and more efficient administration. Hybrid models keep fund operations partially off-chain (for administration and compliance) while issuing on-chain share registers, allowing incremental adoption and regulatory alignment.

Specific fund types suited for tokenization include:

Variable capital companies (VCCs): flexible structures popular in Singapore for pooled investment schemes

Real estate funds: tokenized property portfolios that divide ownership into tradable fractions

Private equity and venture capital funds: traditionally illiquid positions that gain secondary-market access through tokens

Commodities funds: portfolios holding gold, silver, oil, diamonds or other physical commodities

Carbon credit funds: pools of environmental credits that can be tracked and traded on-chain

Infrastructure and debt funds: long-duration assets like toll roads, utilities or loan portfolios that benefit from transparent, automated recordkeeping

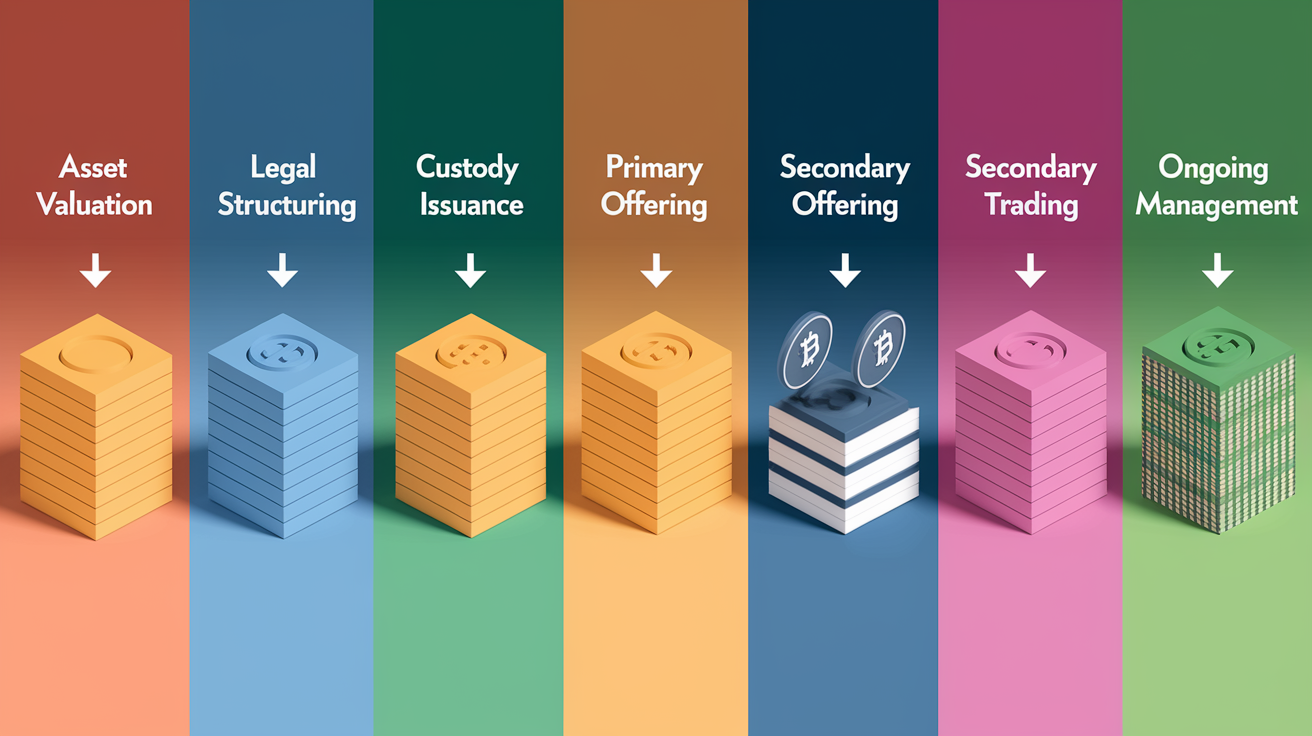

The Full Fund Tokenization Process Explained Step-by-Step

The journey from a traditional fund to a fully operational tokenized vehicle unfolds in seven core stages:

Asset selection and valuation. The fund manager documents the value of the underlying assets using standard financial practices (appraisals, mark-to-market pricing or third-party audits) to establish a baseline NAV.

Legal structuring and token design. Choose a token structure and define token-holder rights. Two common models are tokenized Special Purpose Vehicle (SPV) or indirect tokenization, where the asset is held by an entity (company or trust) and tokens represent pooled investor interests that fit securities regulation more cleanly. Direct asset tokenization, where tokens represent a direct claim on the asset, is less common due to regulatory and non-fungibility challenges.

Custody of real-world assets and tokens. Physical real-world assets (RWAs) are held by qualified custodians or trustees. Digital tokens are held via custody arrangements detailed below.

Token issuance. The fund mints RWA or security tokens on a chosen blockchain (for example, Ethereum) and distributes them via the issuer’s website or a licensed platform.

Primary offering. The initial sale of tokenized securities raises capital. Pricing and investor classes are managed via standard underwriting or placement processes adapted to token form.

Secondary trading. Token-holders can trade their positions on licensed RWA broker-dealers, licensed RWA exchanges or decentralized exchanges (for example, automated market maker–style DEXes), subject to compliance gates and transfer restrictions.

Ongoing management. The fund handles regulatory compliance, tax filings, periodic valuations, dividend or voting events, smart-contract updates, audits and investor relations until maturity or redemption.

Custody Models for Tokenized Funds

Physical RWAs remain in the custody of qualified third parties (banks, trust companies or specialized asset custodians) who provide insurance, audit trails and legal safeguards. Digital tokens, meanwhile, are held either in self-custody wallets, where the investor controls private keys and bears full responsibility for security, or through licensed digital-asset custodians that offer regulated custody using multi-party computation (MPC), multi-signature wallets, hardware security modules (HSMs) and key sharding to protect against single points of failure. Many institutional platforms combine both layers: a traditional custodian for the underlying assets and a regulated crypto custodian for the token layer, ensuring compliance with existing fund rules while delivering blockchain benefits.

Key Benefits of Tokenized Investment Funds for Investors and Issuers

Tokenized funds unlock tangible advantages for all participants. For investors, fractional exposure to high-barrier assets that were once reserved for institutions or ultra-high-net-worth individuals becomes accessible at lower minimums. A tokenized real estate fund might divide a USD 50 million property into 500,000 tokens, each representing a USD 100 stake. Increased liquidity follows from the ability to trade tokens on secondary markets rather than waiting for quarterly redemption windows or fund wind-downs. Better transparency comes from immutable on-chain records that show every transaction, ownership change and corporate action in real time. Faster settlement cuts the typical T+2 cycle to near-instant atomic swaps when both legs of a trade (asset and payment) execute simultaneously on-chain.

For issuers and fund managers, tokenization opens new capital-raising channels and expands the investor base globally, subject to regulatory permissions. Operational automation via smart contracts reduces reconciliation workloads, lowers administration costs and frees staff to focus on portfolio management instead of back-office paperwork. Service providers (custodians, transfer agents, broker-dealers) benefit from reduced reconciliation burdens, near-instant settlement and opportunities to offer specialized custody, trading or compliance-as-a-service solutions.

Fractional ownership lowers entry barriers and broadens diversification. 24/7 transferability (within compliance rules) improves capital mobility. Real-time, auditable records increase trust and simplify reporting. Smart-contract automation cuts costs and shortens timelines.

Risks and Challenges of Tokenized Investment Funds

Regulatory uncertainty sits at the top of most risk lists. Rules differ sharply by jurisdiction, and frameworks continue to evolve. What’s permitted in Singapore or Switzerland might be restricted or unclear in other markets. Market volatility affects tokenized funds just as it does traditional vehicles, but the overlay of crypto-market sentiment can amplify price swings in thinly traded secondary markets. Liquidity constraints remain real: a token doesn’t guarantee a buyer, and illiquid private-fund tokens may trade at steep discounts or not at all if no exchange or market maker supports them.

Smart-contract vulnerabilities present operational and financial risk. Bugs in code can lock funds, enable unauthorized withdrawals or disrupt corporate actions. Thorough audits and formal verification are necessary but not foolproof. Oracle manipulation risk arises when price or NAV feeds are compromised, leading to incorrect valuations and settlement errors. Custody and private-key risks mean that lost keys equal lost assets, and even institutional-grade multi-signature or MPC solutions introduce dependencies on third-party providers and operational processes.

Interoperability challenges and the lack of universal standards hinder cross-chain liquidity and complicate integration with legacy financial systems. Privacy considerations become acute when identity, compliance checks and transaction histories move on-chain. Cryptographic privacy-preserving techniques such as verifiable credentials are necessary to avoid exposing personal data while still meeting Know Your Customer (KYC) and Anti-Money Laundering (AML) obligations. Investor education and trust remain barriers. Many participants lack the technical literacy to manage wallets, understand gas fees or evaluate smart-contract security, slowing adoption outside tech-savvy circles.

Real-World Examples of Tokenized Investment Funds and Institutional Pilots

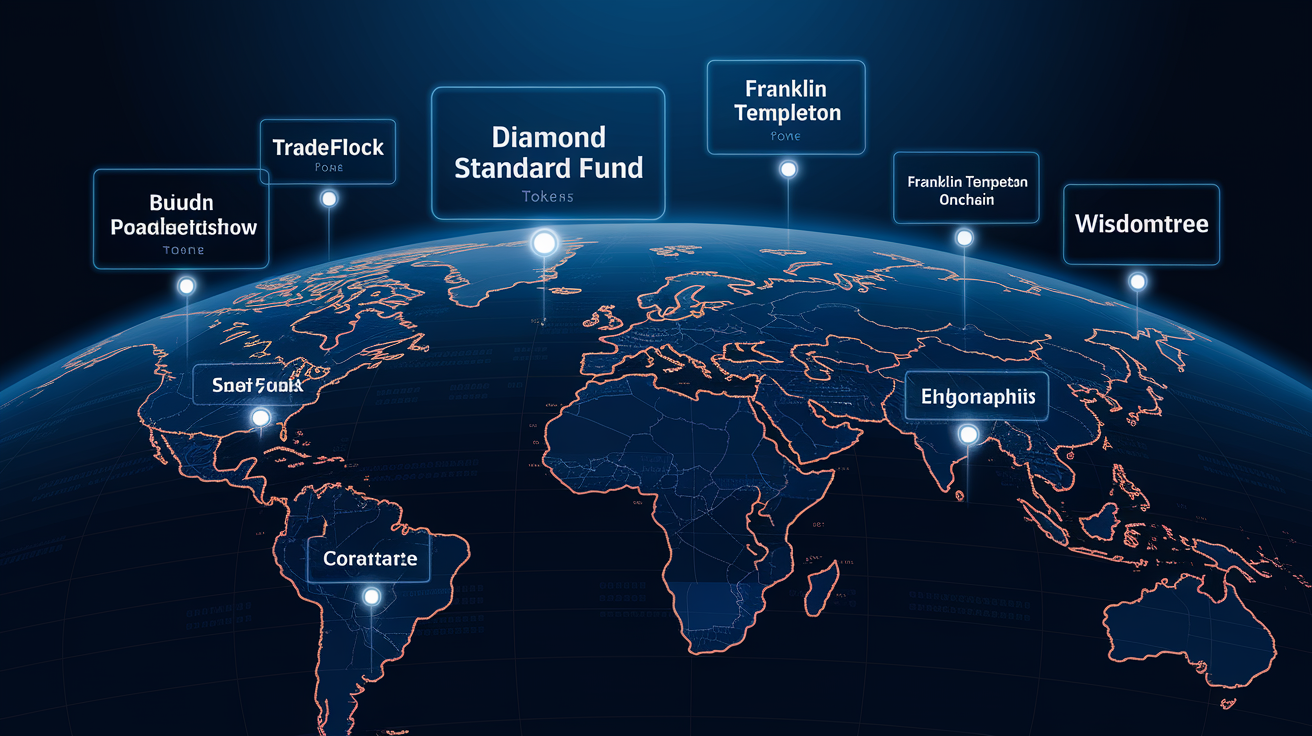

BlackRock launched its BUIDL tokenized money market fund on the Ethereum blockchain in March 2024 and captured nearly 30 percent of a USD 1.3 billion tokenized Treasury market within six weeks. As of November 5, 2025, BUIDL reported assets under management of USD 2,829,107,501, offering U.S. dollar–based yields and redemption options through a digital securities provider. This demonstrates that institutional asset managers can scale tokenized funds rapidly when infrastructure and regulatory clarity align.

TradeFlow Capital, founded in Singapore in 2016, manages roughly USD 100 million in assets and tokenized its commodity trade finance fund to improve accessibility and liquidity. The fund provides exposure to pre-booked, insured commodity transactions through regulated tokenization platforms. Diamond Standard Fund took a different path, tokenizing physical diamond portfolios and listing on a U.S. Securities and Exchange Commission–registered alternative trading system (ATS). The fund’s performance is tracked by the DIAMINDX benchmark published by Bloomberg, and tokenization expanded market access across the United States and Asia.

Hamilton Lane introduced tokenized feeder funds to broaden retail and accredited-investor access to private equity strategies, while Franklin Templeton’s OnChain U.S. Government Money Fund issues and manages shares as digital tokens (a blockchain-based mutual fund that automates subscriptions, redemptions and reporting). WisdomTree is piloting blockchain-enabled mutual funds, exploring operational efficiencies and new distribution channels.

Institutional pilots showcase collaborative innovation and real-world validation:

Monetary Authority of Singapore’s Project Guardian: on-chain share registers demonstrated with UBS Asset Management, SBI Digital Markets and Chainlink, illustrating incremental on-chain adoption across custodians and asset managers

Real-time NAV pilot: Sygnum Bank, Fidelity International and Chainlink published real-time NAV data on-chain for Fidelity’s Institutional Liquidity Fund, proving that on-chain pricing can support timely valuation and settlement for money market products

Atomic DvP and cross-border compliance pilots: Kinexys by J.P. Morgan, Ondo Finance and Chainlink executed an atomic DvP transaction involving tokenized U.S. Treasury fund units and digital payment tokens. Separately, Visa, Fidelity International, ANZ Bank and Chainlink demonstrated compliant cross-border settlement under the Hong Kong Monetary Authority’s e-HKD+ program using on-chain identity and compliance checks

Regulation, Compliance Requirements and Jurisdictional Considerations for Tokenized Funds

Every tokenized fund must navigate the same KYC and AML obligations that govern traditional funds, but on-chain workflows enable embedding compliance rules directly into smart contracts. Investor accreditation checks, jurisdictional blocking and transfer restrictions can be encoded using verifiable credentials and automated compliance engines, allowing proof of eligibility without revealing sensitive personal data. Singapore, Hong Kong SAR and Switzerland emerged as leading jurisdictions for asset tokenization according to KPMG analysis published in October 2023, offering clear regulatory pathways, sandbox programs and supportive infrastructure.

In the United States, the Depository Trust Company received a no-action letter from the SEC permitting a broad three-year pilot to record securities entitlements using distributed ledger technology, signaling regulatory willingness to test tokenized rails at scale. Nasdaq announced preparations for trading tokenized securities in September 2025, and amendments to Regulation S-P mandated incident response, vendor oversight and breach notifications, with compliance required by December 3, 2025, for large firms and June 3, 2026, for smaller firms. The Financial Accounting Standards Board tentatively decided to expand digital-asset guidance, including stablecoin cash-equivalent examples, while pending legislation such as the CLARITY Act is expected to address legal uncertainty around tokenized assets.

Cross-border distribution introduces additional complexity: a token issued in one jurisdiction may not be transferable to residents of another without registration or an exemption, and on-chain whitelisting or geo-blocking becomes necessary to enforce these restrictions programmatically. Hybrid on-chain and off-chain approaches help meet existing regulatory reporting and custody requirements while improving settlement and recordkeeping, balancing innovation with compliance obligations that remain grounded in traditional securities law.

How Investors Can Participate in Tokenized Investment Funds

Getting started with tokenized funds requires navigating both traditional investment processes and new digital infrastructure. Follow these steps:

Verify regulatory status and investor eligibility. Confirm whether the fund is public or private, which jurisdictions it accepts investors from, and whether you meet accreditation or net-worth thresholds.

Choose a platform and review the fund structure. Select a tokenized fund issuer or licensed marketplace. Understand the token’s rights, transfer restrictions, fees, NAV calculation cadence and redemption mechanics.

Set up custody and wallet solutions. Decide between self-custody (you hold private keys and bear security responsibility) or a custodial provider that offers institutional-grade multi-party computation, hardware security modules and insurance. Make sure the solution meets your security and regulatory requirements.

Complete KYC/AML onboarding. Provide identity documents and proof of address. Some platforms issue cryptographic verifiable credentials that prove compliance on-chain without exposing personal data.

Acquire tokens and monitor on-chain data. Subscribe via primary issuance or purchase on approved secondary venues. Track on-chain NAV feeds, smart-contract enforced rules and settlement workflows (atomic DvP versus legacy rails).

Understand tax and reporting obligations. New reporting frameworks and forms such as Form 1099-DA are emerging. Fund managers and investors must plan for reconciliation, documentation and tax compliance in their home jurisdictions.

Operational Best Practices and Infrastructure Considerations for Tokenized Fund Managers

Fund managers adopting tokenization must integrate blockchain capabilities with legacy administration, custody and compliance systems. Start by selecting adoption strategies: self-build a platform (costly, multi-year timeline), partner with a token-issuance-only provider, use a token-exchange-only solution or engage an all-in-one solution provider that handles issuance, custody, trading and lifecycle management. Oracles become mission-critical infrastructure for delivering trusted NAV and pricing data on-chain. Pilots have demonstrated real-time NAV feeds using secure oracle networks, enabling timely valuation and automated settlement.

DvP settlement requires choreographing asset and payment legs across traditional and blockchain rails, often using cross-chain interoperability protocols such as the Cross-Chain Interoperability Protocol (CCIP) and orchestration layers like the Chainlink Runtime Environment (CRE) that translate legacy messaging formats (ISO 20022, Swift) into on-chain workflows. Emerging standards such as the Digital Transfer Agent (DTA) specification, Automated Compliance Engine (ACE) and Cross-Chain Identity (CCID) provide reusable frameworks for share registers, embedded compliance and verifiable credentials, reducing custom development and improving interoperability.

Conduct regular smart-contract audits and penetration testing to catch vulnerabilities before launch. Secure custody insurance and operational risk coverage for both digital and physical asset layers. Budget for ongoing compliance, technology updates and investor education. Tokenization isn’t a one-time implementation. Plan lifecycle management tasks: NAV publication, distribution automation, voting, regulatory reporting and smart-contract governance upgrades.

Future Outlook for Tokenized Investment Funds and Market Adoption Trends

Institutional pilots conducted across 2024, 2025 and into early 2026 have demonstrated functional advantages (real-time NAV, atomic DvP, on-chain compliance) but broad adoption depends on regulatory alignment, standards maturation and integration with legacy financial rails. Rising interoperability standards, growing regulatory clarity in key jurisdictions and improving infrastructure maturity are accelerating the shift from proof-of-concept to production deployment. Major asset managers, custodians and market infrastructure providers are investing in tokenization capabilities, signaling that tokenized funds will expand across asset classes over the next several years.

Remaining obstacles include liquidity depth (secondary markets for tokenized private funds remain thin) and the lack of universal cross-chain standards, which fragments liquidity and complicates multi-platform participation. Interoperability solutions and standardized protocols such as DTA, ACE and CCIP are expected to reduce friction, but widespread adoption will require years of iterative development, regulatory evolution and user education. The industry snapshot from 2025 through early 2026 shows momentum building: tokenized money market funds crossing billions in AUM, regulated pilots clearing regulatory hurdles and infrastructure providers scaling commercial offerings.

Final Words

We jumped straight into how tokenized funds work: fund shares become blockchain tokens, they enable fractional ownership, and smart contracts automate actions. We covered types, the seven-step tokenization process, custody models, and real pilots.

We also explained benefits, risks, regulation, how investors join, and manager best practices. The goal was practical, not theoretical.

If you still ask “what are tokenized investment funds and how they work”, the short answer is that they turn fund ownership into on-chain tokens, keeping the same economics while adding fractional access, faster settlement, and tradeability. It’s early but promising, so start small and stay curious.

FAQ

Q: What are tokenized investment funds and how do they work?

A: Tokenized investment funds are funds whose shares are digital tokens on a blockchain. They convert ownership on‑chain, enable fractional ownership, use smart contracts for operations, oracles for NAV, and atomic DvP; industry AUM ≈ USD 147T (mid‑2025).

Q: What types of funds and assets can be tokenized?

A: Tokenized funds can be public (ETFs, mutuals), private (PE, VC, private credit, real estate), or hybrid. Assets include real estate, commodities, gold, silver, oil, diamonds, carbon credits, debt, hedge and infrastructure funds.

Q: What are the main steps in the fund tokenization process?

A: The main steps are asset selection and valuation; legal structuring (direct or SPV); custody choice; token issuance and primary offering; secondary trading; oracle‑fed NAV and DvP settlement; ongoing reporting, audits, and smart‑contract updates.

Q: What custody models are used for tokenized funds?

A: Custody models for tokenized funds include physical RWA custody for underlying assets, digital token custody options like self‑custody, MPC (multi‑party computation), multi‑sig, HSMs, and licensed custodial providers.

Q: What are the main benefits of tokenized investment funds?

A: The main benefits of tokenized funds are fractional ownership, wider global access, faster 24/7 settlement, lower operational costs from automation, real‑time records, composability, and immutable audit trails.

Q: What risks and challenges do tokenized investment funds face?

A: The risks for tokenized funds include regulatory uncertainty, smart‑contract bugs and oracle manipulation, custody and private‑key risks, limited liquidity, interoperability gaps, privacy trade‑offs, infrastructure shortfalls, and investor education needs.

Q: How do investors start with tokenized funds?

A: To start with tokenized funds, verify eligibility and platform rules, complete KYC/AML, set up secure custody or wallet, subscribe on primary or buy on secondary venues, monitor on‑chain NAV, and track tax reporting.

Q: What regulatory and jurisdictional issues affect tokenized funds?

A: Regulatory issues for tokenized funds include KYC/AML, investor eligibility and whitelisting, cross‑border distribution limits, jurisdiction differences (Singapore, Hong Kong, Switzerland leading), DTC pilots, and pending rules like Reg S‑P deadlines.

Q: What notable real-world tokenized fund pilots and launches exist?

A: Notable pilots include BlackRock BUIDL (March 2024; AUM $2,829,107,501 as of Nov 5, 2025), TradeFlow Capital, Diamond Standard, Hamilton Lane feeders, Franklin Templeton OnChain, and MAS/Chainlink atomic DvP and NAV pilots.

Q: What operational best practices should tokenized fund managers follow?

A: Managers should integrate blockchain with legacy rails, use oracles for NAV, enable DvP settlement, follow smart‑contract audits, secure custody insurance, adopt lifecycle management standards, and plan cost and admin workflows.

Q: What is the future outlook for tokenized investment funds?

A: The outlook for tokenized funds shows growing institutional pilots and clearer rules across 2024–2026, improving infrastructure and standards, broader asset expansion, but remaining liquidity, cross‑chain and standardization challenges.